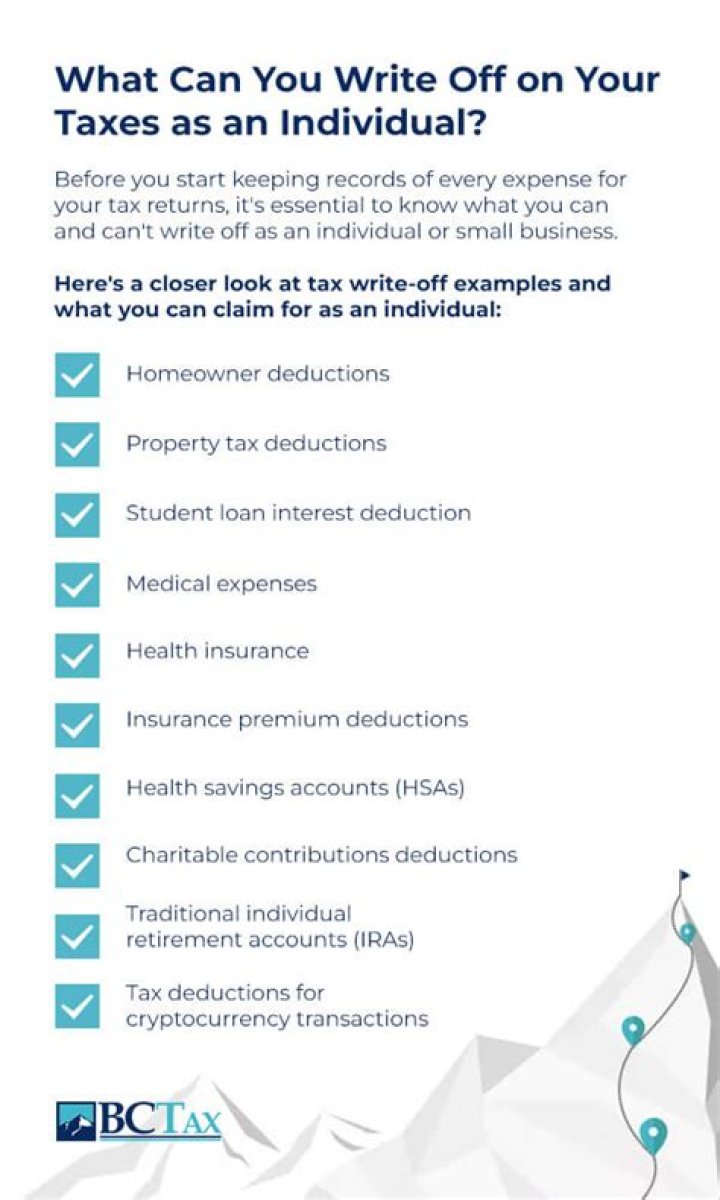

What is the difference between ho2 ho3 homeowners insurance

Christopher Martinez

Christopher Martinez In total, it covers 16 perils. The HO2 provides more protection than the HO1, but not as much as an HO3, and similar to an HO1, a HO2 policy also excludes coverage for floods and earthquakes.

Is HO3 or HO2 better?

In total, it covers 16 perils. The HO2 provides more protection than the HO1, but not as much as an HO3, and similar to an HO1, a HO2 policy also excludes coverage for floods and earthquakes.

Does HO2 cover water damage?

While HO2 does offer broader coverage than HO1, it still excludes some common risks you may face. For instance, HO2 includes sudden and accidental discharge of water and steam but usually omits sewer backup and slow leaks. HO-2 also excludes coverage for: Floods.

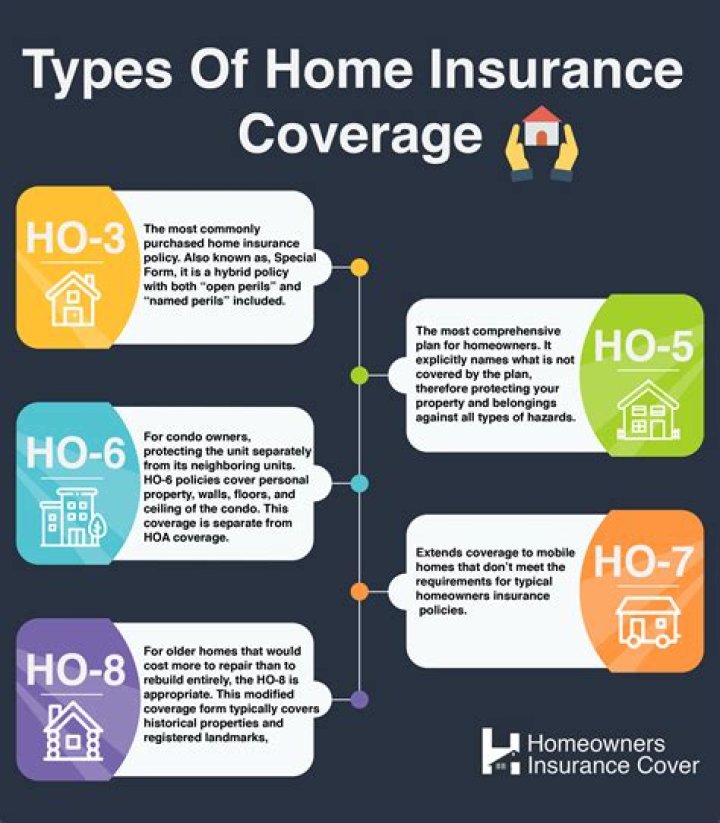

What is an HO 3 homeowners policy?

Homeowners Policy Special Form 3 (HO 3) — part of the Insurance Services Office, Inc. (ISO), homeowners forms portfolio, the HO 3 insures the described owner-occupied dwelling, private structures in connection with the dwelling, unscheduled personal property on and away from the premises, and loss of use.What is an HO 9 policy?

Schedule I (HO-9) Schedule I insurance is used for older homes. It is often a Schedule C policy with special provisions for leaky plumbing coverage, electrical systems coverage and insect damage, although it can be tweaked to account for any area-specific peril.

What does DP 3 insurance cover?

A DP3 policy covers the structure, loss of use or rental coverage, and usually personal liability. … Additional items that may not be covered by a DP3 product can include other structures, such as a garage or shed. Lighthouse DP3 does provide replacement cost coverage on the dwelling up to your policy limit.

What is HO2 form?

An HO-2 policy, also known as a broad form policy, is a type of homeowners insurance that contains more coverage than the most basic of policy forms but less coverage than a standard HO-3 policy. An HO-2 provides coverage for your home and personal property against 16 named perils.

What is an HO-5?

HO-5 policies provide premium coverage for owner-occupied homes. Most HO-5 policies provide open-peril coverage for your home and its contents. That means that your home and personal property are equally protected. However, like an HO-3 policy, HO-5 coverage comes with exclusions.Is an HO 3 policy replacement cost?

One of the big benefits of an HO3 policy is that it offers replacement cost coverage for your home and other structures.

Does HO3 cover wind and hail?Question # 1: Am I covered for direct losses due to fire, lightning, tornadoes, wind storms, hail, explosions, smoke, vandalism and theft? Answer: Yes. The HO-3 provides broad coverage for these and other disasters or “perils,” as they are called in the policy, including all those listed in the question.

Article first time published onDoes HO3 cover flood?

HO-3 insurance is the most popular type of home insurance policy. HO-3 covers your dwelling under an open peril policy, and your personal items under a named peril policy. HO-3 insurance does not cover earthquakes, floods, wear and tear, and negligence, among other things.

What is the difference between HO1 and HO3?

HO1 and HO2 policies are examples of “named perils policies.” That means they only cover dangers that are specifically listed in the policy. HO3 policies are “open peril policies”. That means they’ll cover all dangers except those specifically excluded in the policy documents.

What water damage is covered in homeowners insurance?

When water damage is covered by homeowners insurance: Rain or snow storm. Plumbing: burst pipes, frozen plumbing, faulty plumbing, accidental overflow. Water damage from extinguishing a fire. Leaking roof (coverage would apply only to the home interior, not the roof itself)

What are the three main types of property insurance coverage?

Understanding Property Insurance There are three types of property insurance coverage: replacement cost, actual cash value, and extended replacement costs.

What is an HO 1 policy?

An HO-1, or “basic form,” is a policy that typically helps cover 10 perils (compared with the 16 perils covered by an HO-3). For example, falling objects or the weight of ice are perils not covered by an HO-1 form, the III says.

What are the 11 perils?

Basic form covers these 11 “perils” or causes of loss: Fire or Lightning, Smoke, Windstorm or Hail, Explosion, Riot or Civil Commotion, Aircraft (striking the property), Vehicles (striking the property), Glass Breakage, Vandalism & Malicious Mischief, Theft, and Volcanic Eruption.

Which of the following homeowners Forms is designed for a condominium unit owner?

The HO-6—Unit-Owners Form (HO 00 06), or HO-6, provides coverage for personal property on a named perils basis, with limited dwelling coverage (unit improvements and betterments). The HO-6 is designed to meet the risk management needs of the owners of condominium units and cooperative apartment shares.

Which of the following homeowners coverage does not have a deductible?

Which of the following homeowners coverage does not have a deductible? Damage to property of Others is an Additional Coverage under Section II, which is not subject to a deductible. A guest falls in K’s house and is injured in an amount of $1,000.

What type of insurance is HO8?

Homeowners Modified Form 8 (HO 8) — part of the Insurance Services Office, Inc. (ISO), homeowners portfolio, the HO 8 form provides basic named perils coverage for direct damage to property, personal liability coverage, and medical payments to others as respects owner-occupied dwellings.

What is the difference between HO3 and DP3?

The DP3 refers to an insurance policy covering a residential building, usually rented to others. The HO3 is reserved for homeowners, but not exclusively single-family homes. … If the owner insures a rental property with an HO3 but lives elsewhere, it’s a bad fit; you risk NOT being covered for losses.

What is the difference in perils between the DP 2 and DP 3?

DP3 Insurance is All Risk Insurance The DP 1 and DP 2 are named peril policies, while the DP 3 is an open peril policy. Named peril insurance policies are policies that specifically list the perils that are insured under the policy.

What is the difference between a DP1 and a DP3?

The DP1 and DP3 are two types of dwelling fire policies. The DP1 is used for vacant property insurance and offers the minimum coverage amount while the DP3 is for landlord insurance where the homeowner rents out the property, but does not live there.

Is a HO3 policy ACV or RCV?

RCV Differences. HO-3 policies reimburse you for damaged property based on the property’s ACV or actual cash value. … In contrast, HO-5 policies reimburse you based on the RCV or replacement cost value of your property.

What's not protected by most homeowners insurance?

Termites and insect damage, bird or rodent damage, rust, rot, mold, and general wear and tear are not covered. Damage caused by smog or smoke from industrial or agricultural operations is also not covered. If something is poorly made or has a hidden defect, this is generally excluded and won’t be covered.

Which of the following is excluded by the Ho-3 form?

Typically, the following are excluded on an open peril policy: Freezing pipes and systems in vacant dwellings. Damage to foundations or pavements from ice and water weight. Theft from a dwelling under construction.

What is the difference between HO3 and HO5 insurance?

HO5 policies cover your contents at replacement cost. This means you’ll be paid enough money to buy a new item. An HO3 policy pays you actual cash value for your contents. This takes into account depreciation and pays you the amount your items would sell for on the open market.

Does HO3 cover roof replacement?

If you have an HO-3 policy, it likely will cover roof damage caused by ice buildup but may exclude personal property damages caused in the same disaster.

Does home insurance cover roof damage from wind?

Yes, as noted above, homeowners insurance typically covers most types of wind damage. Usually, the dwelling coverage of your homeowners policy will help pay to repair or replace damage to the roof, siding or windows due to a wind event.

How much wind and hail insurance do I need?

State and federal laws do not require you to have wind or hail insurance. Mortgage companies may require you to carry it if your homeowners insurance coverage excludes it, though. Even when it is not required, it should be a serious consideration for those who live in an area prone to wind and or hail.

How does insurance work if your house burns down?

Your homeowner’s insurance will likely cover items destroyed in a house fire. If you have a replacement cost policy, you’ll receive the actual cash value of your damaged items at the time of settlement [Replacement Cost – Depreciation = Actual Cash Value].

Are acts of God covered by homeowners insurance?

Many standard homeowners insurance policies cover natural disasters, which means hurricanes, tornados and lightning storms can be covered. Act of God events caused by floods or earthquakes are not covered under standard homeowners policies. … Remember, most homeowners insurance covers common acts of god.