When can you refinance from FHA to conventional

John Peck

John Peck You can refinance an FHA loan to a conventional loan if you meet the minimum requirements for a conventional mortgage, which differ from FHA requirements.

Can you refi from FHA to conventional?

You can refinance an FHA loan to a conventional loan if you meet the minimum requirements for a conventional mortgage, which differ from FHA requirements.

How long do you have to have an FHA loan before you can refinance?

How soon can you refinance an FHA loan? You must have owned your home for 210 days — or seven months — and made on-time payments for at least six months before you can refinance using an FHA streamline.

Can you switch from FHA to conventional?

To convert an FHA loan to a conventional home loan, you will need to refinance your current mortgage. The FHA must approve the refinance, even though you are moving to a non-FHA-insured lender. The process is remarkably similar to a traditional refinance, although there are some additional considerations.What credit score do I need to refinance from FHA to conventional?

Loan TypeFHA LoanMinimum Credit Score500-580

Is Conventional better than FHA?

FHA loans allow lower credit scores than conventional mortgages do, and are easier to qualify for. Conventional loans allow slightly lower down payments. … FHA loans are insured by the Federal Housing Administration, and conventional mortgages aren’t insured by a federal agency.

How do I get rid of my FHA PMI?

Getting rid of PMI is fairly straightforward: Once you accrue 20 percent equity in your home, either by making payments to reach that level or by increasing your home’s value, you can request to have PMI removed.

Do conventional loans require PMI?

If you put down less than 20% on a conventional loan, you’ll be required to pay for private mortgage insurance (PMI). PMI protects your lender in case you default on your loan. The cost for PMI varies based on your loan type, your credit score and the size of your down payment.How much equity do I need to refinance to a conventional loan?

Strictly speaking, you only need 5 percent equity in some cases to get a conventional refinance. However, if your equity is less than 20 percent, then you’ll likely face higher interest rates and fees, plus you’ll have to take out mortgage insurance. Most lenders want you to have at least 20 percent equity.

Is an FHA loan considered conventional?An FHA loan is a government-backed home loan insured by the Federal Housing Administration. An FHA loan has less-restrictive qualifications compared to a conventional loan, which is not backed by a government agency.

Article first time published onCan you refinance an FHA mortgage after 6 months?

You must have made at least six payments on your FHA mortgage. At least 6 full months must have passed since the first payment was due on the mortgage. At least 210 days must have passed from the closing date of the mortgage you’d like to refinance.

How hard is it to get a conventional loan?

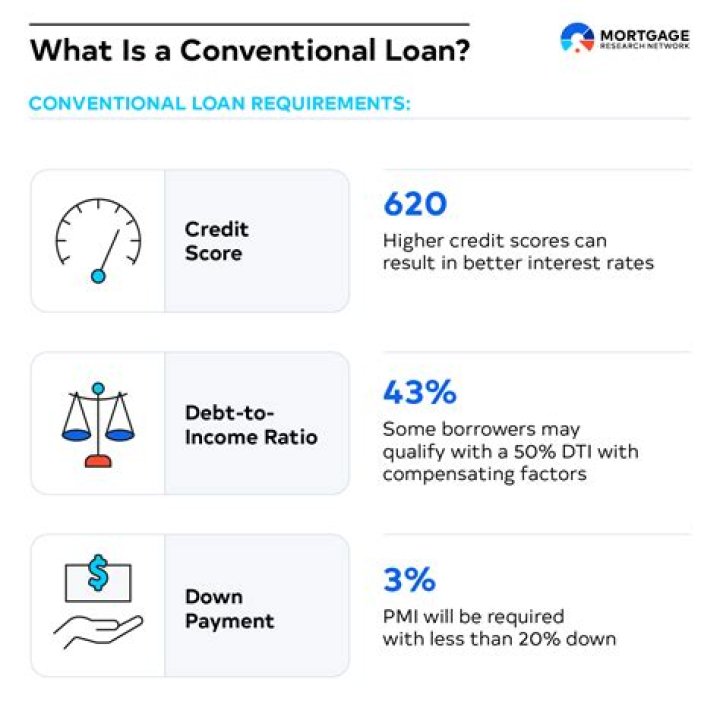

Even though a conventional loan is the most common mortgage, it is surprisingly difficult to get. Borrowers need to have a minimum credit score of about 640 in order to qualify—the highest minimum score of all mortgage products—and have a debt-to-income ratio of 43% or less.

How much does it cost to refinance into a conventional loan?

It can cost between 2% and 6% of the loan amount to refinance a conventional loan. These refinances can have higher credit and financial requirements compared to other mortgages. However, you can get competitive interest rates when you have a good credit score and personal finances.

Can I refinance with a 650 credit score?

In general, a credit score of 670 or above is considered good, scores between 580 and 669 are considered fair and anything below 580 is considered poor. When it comes to the credit score needed to refinance, 620 tends to be the minimum for a conventional loan.

Do FHA loans have PMI forever?

Despite what you’ve heard, FHA mortgage insurance premium (MIP) is not permanent. … With mortgage rates near historic lows, and home values rising, many are choosing to refinance. Getting rid of FHA MIP is a big deal. You can check your eligibility for a new, PMI–free mortgage via a refinance.

Are conventional loan rates higher than FHA?

Conventional loan interest rates are typically a little higher than FHA mortgage rates. That’s because FHA loans are backed by the Federal Housing Administration, which makes them less “risky” for lenders and allows for lower rates.

Is FHA PMI permanent?

The good change is that FHA lowered its mortgage insurance premiums in January 2015. On the negative side, they’ve made PMI essentially permanent over the life of most mortgages that they insure.

Can I refinance my conventional loan?

Refinancing a conventional loan can position you to reduce your current monthly expenses. … Conventional loan programs can provide options for a homeowner to change his current mortgage terms by refinancing. A lender or mortgage broker can assist you with refinancing your conventional mortgage.

Can you put 3 down on a conventional loan?

Can I get a mortgage with 3% down? Yes! The conventional 97 program allows 3% down and is offered by many lenders. Fannie Mae’s HomeReady loan and Freddie Mac’s Home Possible loan also allow 3% down with extra flexibility for income and credit qualification.

What credit score do you need for a conventional loan?

According to mortgage company Fannie Mae, a conventional loan usually requires a credit score of at least 620. But you may qualify for a government-sponsored loan with a lower score. Read on to learn more about credit scores and how they impact the homebuying process.

How do you qualify for a conventional refinance?

To qualify for a conventional loan, you’ll typically need a credit score of at least 620. Borrowers with credit scores of 740 or higher can make lower down payments and tend to get the most attractive conventional loan rates, however.

Why is my loan amount higher after refinancing?

Home loan interest is tipped toward the early years. … If you’ve had your loan for a while, more money is going to pay down principal. If you refinance, even at the same face amount, you start over again, initially paying more on interest. That, in effect, increases your mortgage.

What should you not do when refinancing?

- 1 – Not shopping around. …

- 2- Fixating on the mortgage rate. …

- 3 – Not saving enough. …

- 4 – Trying to time mortgage rates. …

- 5- Refinancing too often. …

- 6 – Not reviewing the Good Faith Estimate and other documentats. …

- 7- Cashing out too much home equity. …

- 8 – Stretching out your loan.

Can you buy a fixer upper with a conventional loan?

You can certainly buy a fixer-upper with a conventional loan, and many people do, but you’ll still need a plan on how you’ll finance the renovations. … This loan type allows you to combine both the purchase and renovation of the property into one long-term, fixed-rate mortgage.

Does conventional loan require appraisal?

One of the main requirements for a conventional loan is that the home must be appraised. The appraiser’s job is to work out the property’s actual market value. Usually, they do this by comparing the property with other, similar homes in the neighborhood that have sold recently.

Is it better to put 20 down or pay PMI?

PMI is designed to protect the lender in case you default on your mortgage, meaning you don’t personally get any benefit from having to pay it. So putting more than 20% down allows you to avoid paying PMI, lowering your overall monthly mortgage costs with no downside.

Are conventional loans government backed?

Conventional Loans: An Overview. Consumers qualify for various types of mortgages based on their financial profiles. … These loans are generally offered by private mortgage lenders like banks, credit unions, and other private companies. Unlike FHA loans, conventional mortgages aren’t backed or secured by the government.

Can I refinance immediately after closing?

Refinancing soon after you close on your mortgage is possible, though you may need to wait up to 24 months in some cases. A mortgage refinance allows you to replace your current mortgage with a new loan to seek better terms. … Even if you’re just a few months into your mortgage, you might be able to refinance right now.

What are the pros and cons of a conventional loan?

- Credit Considerations. Riskier than mortgages backed by the US government, conventional loans typically hold borrowers to a higher standard. …

- Money Down & Mortgage Insurance. …

- More Options. …

- Time & Cost to Close. …

- A Seller’s Market.

Is a conventional loan a fixed rate?

Conventional loans typically come with fixed interest rates, with the option to refinance later. A higher credit score will yield you a lower interest rate.

How much does it cost to refinance a mortgage 2021?

How much does it cost to refinance a mortgage in 2021? Generally speaking, you should expect to pay anywhere from 2% to 5% of the amount of your new loan when you refinance. This means that if you’re taking out a new $200,000 mortgage, you should expect to be charged $4,000 to $10,000 in closing costs.