What is the percentage of completion method in GAAP

Andrew Campbell

Andrew Campbell Percentage of completion (PoC) is an accounting method of work-in-progress evaluation, for recording long-term contracts. GAAP allows another method of revenue recognition for long-term construction contracts, the completed-contract method.

Does GAAP use percentage of completion method?

Construction and engineering contracts normally use the percentage of completion method for revenue recognition. … GAAP also allows the completed contract method, in which a contractor don’t recognize expenses or revenues until the contract is finished.

Who must use percentage of completion method?

- if the contractor’s average annual revenue for the last three years exceeds an exception limit.

- if completion is expected to take at least two years from the date the contract begins.

What is the percentage of completion recognition method?

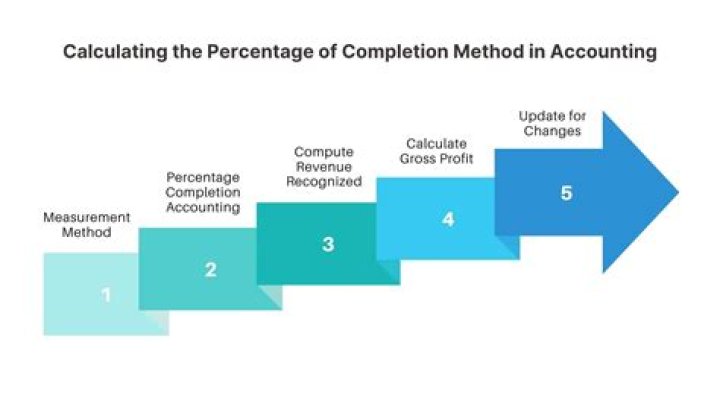

What Is the Percentage of Completion Method? The percentage of completion method is an accounting method in which the revenues and expenses of long-term contracts are recognized as a percentage of the work completed during the period.Does IFRS use percentage of completion method?

The percentage of completion method falls in-line with IFRS 15, which indicates that revenue from performance obligations recognized over a period of time should be based on the percentage of completion. The method recognizes revenues and expenses in proportion to the completeness of the contracted project.

What is percentage of completion method of recognizing income in long-term construction contract?

The percentage of completion method calculates the ongoing recognition of revenue and expenses related to longer-term projects based on the proportion of work completed. By doing so, the seller can recognize some gain or loss related to a project in every accounting period in which the project continues to be active.

What is the percentage of completion method quizlet?

The percentage-of-completion method recognizes gross profit over the production period. … The completed-contract method only recognizes gross profit at the end of the contract.

What is an Underbilling and how is it used in percentage of completion accounting?

From an accounting standpoint, underbilling is the cost and profit earned on a lump-sum construction project that has been incurred within a billing cycle but has not been billed. For example, a contractor completes 90% of a construction project but only bills for 70% of the overall contract. That’s a 20% underbilling.How do you calculate project completion percentage?

Percent Complete is a field that is calculated based on Actual Duration and Duration and it indicates how much progress has been made on the project or on tasks. How is % complete calculated? The % complete has the following formula % complete=(Actual Duration/Duration)*100.

How do you calculate gross profit using percentage completion method?The Percentage of completion formula is very simple. First, take an estimated percentage of how close the project is to being completed by taking the cost to date for the project over the total estimated cost. Then multiply the percentage calculated by the total project revenue to compute revenue for the period.

Article first time published onWhy is percentage of completion better than completed contract?

Percentage-of-Completion Method In contrast to the completed-contract method, the percentage-of-completion provides that revenues, costs, and gross profits be recognized through the income statement as the project is being completed instead of all at the end.

What are the major reasons that the percentage of completion method is such a common accounting method for general contractors?

You will see the percentage of completion method more frequently in construction accounting, as it directly ties revenue and expenses to the project’s completion. It offers construction companies a more accurate view of their financial status over the long-term and more manageable tax liability.

What is the difference between zero profit method and percentage of completion method in long-term construction?

Percentage of Completion Method – with dependable estimates or known as cost to cost method. Zero Profit- with no dependable estimates.

Does IFRS 15 replace IAS 11?

IFRS 15 replaces IAS 11, IAS 18, IFRIC 13, IFRIC 15, IFRIC 18 and SIC‑31. IFRS 15 provides a comprehensive framework for recognising revenue from contracts with customers.

When accounting for a long-term construction contract under IFRS if the percentage of completion method is not appropriate the seller should account for revenue using?

When accounting for a long-term construction contract under IFRS, if the percentage-of-completion method is not appropriate, the seller should account for revenue using: The cost recovery method.

What is the percent complete in construction?

The total percentage of costs that have been incurred is the percentage of completion for the project. Total costs to date ÷ total estimated costs = percent complete.

How do you calculate construction percentage?

- Revenue to be recognized = (Percentage of Work Completed in the given period) * (Total Contract Value)

- Percentage of work completed = (Total Expenses incurred on the project till the close of the accounting period. …

- Example 1 (Continued):

- Year 1.

- Year 2.

- Year 3.

- Year 4.

How do you calculate construction in progress?

Subtract your estimated costs from your contract price to find estimated gross profit. In the example, $200,000 minus $150,000 equals estimated gross profit of $50,000. Multiply your percent complete by your estimated gross profit to find your construction in progress.

How do you calculate percentage completion in Excel?

- Enter the formula =C2/B2 in cell D2, and copy it down to as many rows as you need.

- Click the Percent Style button (Home tab > Number group) to display the resulting decimal fractions as percentages.

How do you calculate total project completion?

When you have calculated the duration of the critical path, you can determine what the expected time of project completion is. Adding the time it takes to complete the tasks on the critical path to the starting date gives you the completion date according to the time estimation definition, says 2020 Project Management.

Is it better to be overbilled or underbilled?

Billings in excess must be monitored, otherwise overbilling and underbilling could pose dangers to a company’s financial stability. Large underbillings can point to slow billing practices, unapproved change orders in the original contract and inaccurate estimates about the costs needed to complete a project.

What are overbillings and Underbillings?

Underbilling is the opposite of overbilling and occurs when a contractor completes a certain amount of work during a billing cycle on a project, but does not bill their customer for the entire amount of work completed during the cycle.

How do you calculate Overbillings?

Overbilling. The amount of billings in excess of progress is simply the amount earned subtracted from the amount billed (H-G).

Is percentage of completion allowed for tax?

The 10-percent method is the percentage of completion method, modified so that any item which would otherwise be taken into account in computing taxable income with respect to a contract for any taxable year before the 10-percent year is taken into account in the 10-percent year.

What is the weakness of the percentage of completion method for recognizing revenue?

The primary disadvantage of this method is that the contractor does not necessarily recognize income in the period earned. This can create additional tax liability since the entire revenue for the project will occur in one period for tax reporting purposes.

Which method of revenue recognition is more conservative?

Method 4: Cost Recoverability This is the most conservative revenue recognition method of all. The cost recoverability approach is used when a company cannot reasonably estimate the total expense required to complete a project.

Is ASC 605 still relevant?

The Financial Accounting Standards Board (FASB) recently amended the rules for revenue recognition in the Accounting Standards Codification (ASC) to add ASC 606: Revenue from Contracts with Customers. This addition will replace ASC 605: Revenue Recognition as well as most industry specific guidance.

What is revenue recognition ASC 606?

ASC 606 is the new revenue recognition standard that affects all businesses that enter into contracts with customers to transfer goods or services – public, private and non-profit entities. Both public and privately held companies should be ASC 606 compliant now based on the 2017 and 2018 deadlines.

What is revenue as per as 9?

As per the AS 9 Revenue Recognition issued by ICAI “Revenue is the gross inflow of cash, receivables or other consideration arising in the course of the ordinary activities of an enterprise from the sale of goods, rendering of services & from various other sources like interest, royalties & dividends”.

How should the balances of progress billings and construction?

The balances of progress billings and construction in process should be shown at net, as a current asset if a debit balance, and as a current liability if a credit balance. >construction costs only.

What is the difference between IFRS 15 and IFRS 16?

With IFRS 15, the price for the smart phone is recognised as revenue as soon as it is handed over to the customer. … IFRS 16 is the ‘leases’ standard and is to be applied as of 1 January 2019, however early application is permitted if adopted with IFRS 15.