What is the meaning of asset impairment

Andrew Campbell

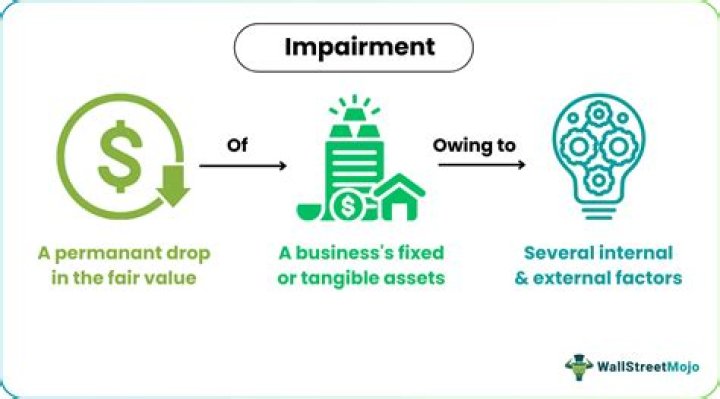

Andrew Campbell Asset impairment is a current market value that is less than the carrying value as recorded on the company’s balance sheet.

What is impairment example?

Impairment in a person’s body structure or function, or mental functioning; examples of impairments include loss of a limb, loss of vision or memory loss. Activity limitation, such as difficulty seeing, hearing, walking, or problem solving.

What is the meaning of impairment in accounting?

What Is Impairment? In accounting, impairment is a permanent reduction in the value of a company asset. It may be a fixed asset or an intangible asset.

What is impairment loss of assets with example?

Impairment occurs when a business asset suffers a depreciation in fair market value in excess of the book value of the asset on the company’s financial statements. … The technical definition of impairment loss is a decrease in net carrying value of an asset greater than the future undisclosed cash flow of the same asset.How do you know if an asset is impaired?

What Is an Impaired Asset? In the United States, assets are considered impaired when the book value, or net carrying value, exceeds expected future cash flows. This occurs if a business spends money on an asset, but changing circumstances caused the purchase to become a net loss.

What is an investment impairment?

An investment is recognized as impaired when there is no longer reasonable assurance that the future cash flows associated with it will be collected either in their entirety or when due. Entities look for evidence of situations that would indicate impairment.

How does asset impairment affect the financial statements?

The loss will reduce income in the income statement and reduce total assets on the balance sheet. The impairment of an asset reduces its value on the balance sheet.: The cost of an impaired building beyond repair is disclosed as a loss on the income statement.

What is asset impairment SAP?

Introduction on Asset Impairment. The state in which an asset has a market value less than its value listed on the company’s records, especially when the value is unlikely to recover. Impaired assets include bad debt, obsolete equipment and, most especially, goodwill.What is impairment of assets in India?

An asset is carried at more than its recoverable amount if its carrying amount exceeds the amount to be recovered through use or sale of the asset. If this is the case, the asset is described as impaired and this Standard requires the enterprise to recognise an impairment loss.

Why is impairment of assets important?IAS 36 Impairment of Assets seeks to ensure that an entity’s assets are not carried at more than their recoverable amount (i.e. the higher of fair value less costs of disposal and value in use).

Article first time published onWhat causes impairment of assets?

An asset may become impaired as a result of materially adverse changes in legal factors that have changed the asset’s value, significant changes in the asset’s market price due to a change in consumer demand, or damage to its physical condition.

What is receivable impairment?

Trade receivables qualify as financial assets and would be considered impaired if its carrying amounts exceeds its recoverable amount. The principle of impairment is the same for both standards IAS 36 and IAS 39. … Impairment losses should be recognised when they are incurred, rather than as expected; and.

What is impairment of intangible assets?

Impairment occurs when an intangible asset is deemed less valuable than is stated on the balance sheet after amortization.

How do you treat impairment of assets?

An impairment loss is recognised immediately in profit or loss (or in comprehensive income if it is a revaluation decrease under IAS 16 or IAS 38). The carrying amount of the asset (or cash-generating unit) is reduced. In a cash-generating unit, goodwill is reduced first; then other assets are reduced pro rata.

What is asset impairment charge?

An impairment charge is a cost that shows a reduction in the carrying value of a specific asset on a balance sheet. This occurs when an asset’s book value exceeds its fair value in the market according to the Generally Accepted Accounting Principles (GAAP).

What is an impairment test in accounting?

Impairment test is an accounting procedure carried out to find out if an asset is impaired, i.e. whether the economic benefits that the asset embodies have dropped drastically. Under US GAAP, if the carrying value of an asset exceeds the sum of undiscounted expected cash flows of an asset, the asset is impaired.

Does impairment affect cash flow?

Cash Flow statement is not affected by impairment directly as there is no cash transaction taking place at the time of impairment. However, it directly affects the income statement and balance sheet directly.

Can impairment loss be reversed?

An impairment loss may only be reversed if there has been a change in the estimates used to determine the asset’s recoverable amount since the last impairment loss had been recognised. If this is the case, then the carrying amount of the asset shall be increased to its recoverable amount.

What is the difference between impairment and write off?

An impairment in accounting is a permanent reduction in the value of an asset to less than its carrying value. An inventory write-off is an accounting term for the formal recognition of a portion of a company’s inventory that no longer has value.

What is impairment of fixed assets?

Impairment of a fixed asset refers to an abrupt decrease in the economic benefits that an asset can generate due to damage, obsolescence etc. Impairment is recognized by reducing the book value of the asset in the balance sheet and recording impairment loss in the income statement.

Is impairment an accounting estimate?

They are used in the financial statements to determine the carrying amounts of assets and liabilities and the associated income or expense for the period where such amounts cannot be measured with precision and certainty. Examples of accounting estimates include: … Impairment of non-current assets.

How often should assets be tested for impairment?

The goodwill of a reporting unit should be tested for impairment on an annual basis, which can be performed at the same time in each succeeding year. It is not necessary to test all reporting units at the same time.

What is impairment as per ind as 36?

An asset is carried at more than its recoverable amount if its carrying amount exceeds the amount to be recovered through use or sale of the asset. If this is the case, the asset is described as impaired and the Standard requires the entity to recognise an impairment loss.

What is impairment loss as per AS 36?

An impairment loss is the amount by which the carrying amount of an asset or a cash-generating unit exceeds its recoverable amount. The recoverable amount of an asset or a cash-generating unit is the higher of its fair value less costs of disposal and its value in use.

How do you calculate impairment loss?

- Subtract the fair market value of the asset from the book value of the asset. …

- Determine if you are going to hold on and use the asset or if you are going to dispose of the asset.

How do you post impairment?

– Post impairment asset: Tcode ABAW: Now, go to tcode ABAW, select the asset to be impaired. Put the transaction type as Z81, press Enter. In the next screen give an asset value date, amount to be posted as Impairment.

What is the accounting for goodwill?

Goodwill is an intangible asset that accounts for the excess purchase price of another company. … Goodwill is calculated by taking the purchase price of a company and subtracting the difference between the fair market value of the assets and liabilities.

Why is impairment important in accounting?

The asset impairment practice ensures that assets are reported on the balance sheet at their fair market value. The practice better reflects the financial picture of a company’s assets for users of the financial statements. Asset impairment can also smoothen the loss of sales when the asset is disposed of.

When should you do an impairment test?

The impairment test is done to find out if the carrying amount of the asset exceeds the recoverable value. … At the time of the acquisition, the carrying amount of an asset equals its original cost price. The company must conduct tests at each balance sheet date that if the asset is impaired.

Does impairment loss affect net income?

An impairment loss makes it into the “total operating expenses” section of an income statement and, thus, decreases corporate net income.

How do you record impairment of intangible assets?

Impairment of Goodwill An impairment cost must be included under expenses when the carrying value of a non-current asset on the balance sheet exceeds the asset’s market value subtracted by any transaction costs (recoverable amount). The impairment cost is calculated as follows: carrying value – recoverable amount.