What is the formula for predetermined overhead rate?

Andrew White

Andrew White What is the formula for predetermined overhead rate?

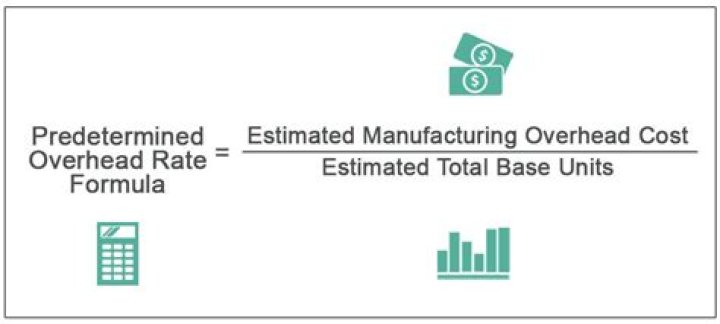

The predetermined overhead rate is set at the beginning of the year and is calculated as the estimated (budgeted) overhead costs for the year divided by the estimated (budgeted) level of activity for the year. This activity base is often direct labor hours, direct labor costs, or machine hours.

How do you calculate predetermined overhead rate using Activity Based Costing?

Calculate the predetermined overhead rate by dividing total overhead costs by total direct labor dollars. Allocate overhead to each type of product by multiplying the overhead cost per direct labor dollar by the per unit direct labor dollars for hollow center balls and for solid center balls.

What is a predetermined rate overhead rate?

A predetermined overhead rate is an allocation rate that is used to apply the estimated cost of manufacturing overhead to cost objects for a specific reporting period. However, the difference between the actual and estimated amounts of overhead must be reconciled at least at the end of each fiscal year.

How is activity rate calculated?

An activity-based costing rate is calculated by assigning indirect costs to a cost pool, adding the costs included in that cost pool together, then dividing the cost pool total by the cost driver.

How do you calculate the predetermined manufacturing overhead rate used to allocate quizlet?

The predetermined manufacturing overhead rate is calculated by multiplying the total estimated manufacturing overhead costs by the total estimated amount of the allocation base. The overhead allocation base should be the cost driver of manufacturing overhead costs.

How do you calculate predetermined overhead rate based on direct labor hours?

An activity base is selected to allocate overhead. This is traditionally direct labor hours, direct labor cost, or machine hours. A predetermined overhead rate is calculated by dividing the estimated overhead by the allocation base.

What is the formula for calculating activity rate?

What is batch level activity?

Batch-level activities are work actions that are classified within an activity-based costing accounting system, often used by production companies. Batch-level activities are related to costs that are incurred whenever a batch of a certain product is produced.

How do you calculate overhead cost per unit?

The overhead cost per unit formula is straightforward and simple: just divide your overhead costs by the number of units sold.

How do you calculate allocated manufacturing overhead?

How to Calculate Overhead Allocation

- Add up total overhead.

- Compute the overhead allocation rate by dividing total overhead by the number of direct labor hours.

- Apply overhead by multiplying the overhead allocation rate by the number of direct labor hours needed to make each product.

Why do companies use a predetermined rate to allocate fixed overhead quizlet?

Some production costs such as a factory manager’s salary cannot be traced to a particular product or job, but rather are incurred as a result of overall production activities. For these reasons, most companies use predetermined overhead rates to apply manufacturing overhead costs to jobs.

What is the formula for the predetermined overhead rate?

The formula for the predetermined overhead rate can be derived by dividing the estimated manufacturing overhead cost by the estimated number of units of the allocation base for the period. Typically, direct labor cost, direct labor hours, machine hours or prime cost is used as the allocation base, while the period usually selected is one year.

What are the alternative denominator activity levels for overhead rates?

There are several alternative denominator activity levels that might be chosen as a basis for the overhead rate calculations. These include: 1) maximum capacity, 2) practical capacity, 3) the normal or long run average production level, and 4) planned production, i.e., master budget units to be produced.

How do you calculate overhead rate variance?

For overhead variance analysis, the standard or pre-determined overhead rate based on total overhead costs is divided into variable and fixed rates, which are calculated by dividing budgeted variable or budgeted fixed overhead by the budgeted allocation base (now referred to as the denominator activity).

What is fixed overhead volume (denominator)?

fixed overhead volume (denominator) variance. measure of utilization of plant facilities. It results when the actual activity level is measured in direct labor-hours, machine-hours, and so on. Differs from the budgeted denominator) uantity used in determining the fixed overhead standard rate.