What is a revocable trust DTD?

Christopher Martinez

Christopher Martinez .

Correspondingly, what is the purpose of a revocable trust?

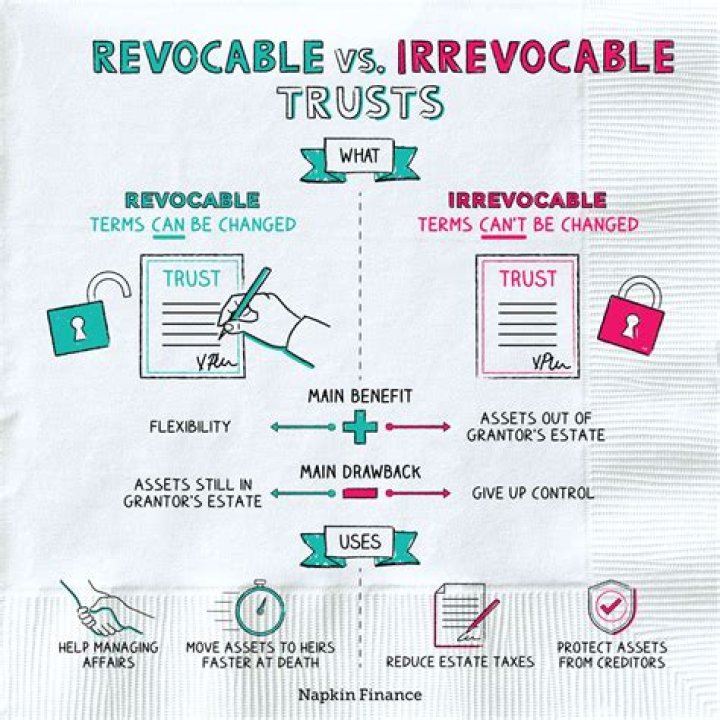

A revocable trust gives the grantor an orderly way to distribute their assets upon their death and privacy for themselves and their heirs during the process.

Secondly, what does DTD mean on a trust? DTD is just an abbreviation for "dated," meaning the date the trust was signed. When referring to a trust, one should always use the date of the trust.

Beside this, who is the beneficiary of a revocable trust?

The person or people benefiting from the trust are the beneficiaries. Because a revocable trust lists one or more beneficiaries, the trust avoids probate.

Can you take money out of a revocable trust?

A revocable trust can be changed, modified or dissolved during the grantor's lifetime. The trustee is the person in charge of distributing the trust assets. If you're named as a beneficiary of the trust, you'll need to communicate with the trustee to withdraw your assets after the grantor's death.

Related Question AnswersWhat are the disadvantages of a revocable trust?

Disadvantages of Revocable Trusts These arise from the different treatment of trusts and wills under certain property laws. As noted, in order to be included in a revocable trust, property must be reregistered in the name of the trust. This may be cumbersome and may involve other costs such as filing fees.What happens to a revocable trust at death?

When the maker of a revocable trust, also known as the grantor or settlor, dies, the assets become property of the trust. If the grantor acted as trustee while he was alive, the named co-trustee or successor trustee will take over upon the grantor's death.When should you have a revocable trust?

Single People. Anyone who is single and has assets titled in their sole name should consider a Revocable Living Trust. The two main reasons are to keep you and your assets out of a court-supervised guardianship and to allow your beneficiaries to avoid the costs and hassles of probate.Why would you set up a revocable trust?

A revocable living trust allows you to provide for the distribution of your property after your death. When you set up a trust, you help your heirs and family avoid the probate courts, which must review and authorize any will. “Revocable” means that you can change the trust at any time, or cancel it altogether.How is a revocable trust taxed after death?

After your death Your final tax return will be filed by your executor or trustee, for income earned through your death. The income earned by trust assets after your passing will be listed on the trust's own, separate income tax return. The trust will need to file an annual fiduciary income tax return (on Form 1041).What assets should be placed in a revocable trust?

Generally, assets you want in your trust include real estate, bank/saving accounts, investments, business interests and notes payable to you. You will also want to change most beneficiary designations to your trust so those assets will flow into your trust and be part of your overall plan.What should you not put in a living trust?

Qualified retirement accounts, including 401(k)s, 403(b)s, IRAs, and qualified annuities, shouldn't reside within your revocable living trust. The reason is the transfer would be treated as a complete withdrawal of funds from your account.Can a nursing home take money from a revocable trust?

A revocable living trust does not protect your assets from nursing home costs. The Home Protection Trust is an irrevocable trust specifically designed to protect its holdings from loss if you ever have to apply for Medicaid to pay for your long term care costs. The trust can sell things held by it, and buy new things.Do revocable trusts file tax returns?

Your Revocable Living Trust at Tax Time In general, you will not have to file IRS Form 1041, the U.S. Income Tax Return for Estates and Trusts, for your revocable living trust—at least not as long as you're alive and well and serving as its trustee.Is a revocable trust worth it?

Revocable trusts are a good choice for those concerned with keeping records and information about assets private after your death. The probate process that wills are subjected to can make your estate an open book since documents entered into it become public record, available for anyone to access.How do I avoid estate taxes?

5 Ways the Rich Can Avoid the Estate Tax- Give Gifts. One way to get around the estate tax is to hand off portions of your wealth to your family members through gifts.

- Set up an Irrevocable Life Insurance Trust.

- Make Charitable Donations.

- Establish a Family Limited Partnership.

- Fund a Qualified Personal Residence Trust.