What are joint costs and how are joint costs recorded?

Christopher Martinez

Christopher Martinez .

Similarly one may ask, what is joint product costing?

Joint costing or by-product costing are used when a business has a production process from which final products are split off during a later stage of production. The point at which the business can determine the final product is called the split-off point.

how do joint costs differ from common costs? Difference between Joint Cost and Common Cost: Joint costs emerge when multiple products are manufactured in a common process and when common inputs are used. Besides common costs can be apportioned to costing objects like products, jobs, department, etc.

One may also ask, should joint costs be allocated among joint products?

Joint costs should not be allocated among joint products for decision-making purposes. If joint costs are allocated among the joint products, then managers may think they are avoidable costs of the end products. Thus, when making decisions about the end products, the joint costs are not avoidable and are irrelevant.

How does the physical measure method allocate joint costs?

The physical measure method allocates cost by the weight, volume, or some other measurement of the product that's produced. It's a contrast to relative sales value. In this case, assume that the weight or volume for each two-by-four is the same. So you allocate joint costs based on the number of units produced.

Related Question AnswersWhat is joint product example?

Joint products are two or more products that are generated within a single production process; they cannot be produced separately and incur undifferentiated joint costs. Examples of join products include: Milk – butter, cream, cheese. Crude oil – fuel, gas, kerosene.What is joint process?

A joint process is a production process in which one input yields multiple outputs. It is a process in which seeking to create one type of output product automatically also creates other types of output product.What is joint product and byproduct?

By-Product. Meaning. When the production of two or more products of similar value, are made together with same input and process, is called joint product. The term by-product means a product which is incidentally produced, during the processing operation of another product.Which joint cost allocation method is best?

The splitoff method in cost accounting Allocating joint costs using sales value at splitoff may be the most effective method for planning and budgeting for joint costs. Here are several reasons why: The method relates the benefit of production (revenue of sales value at splitoff) to the related expenses.Can a byproduct ever become a joint product?

A byproduct has a low total sales value at the splitoff point. Products can change from byproducts to joint products when their total sales values increase significantly.What do you mean by target costing?

It involves setting a target cost by subtracting a desired profit margin from a competitive market price. A target cost is the maximum amount of cost that can be incurred on a product, however, the firm can still earn the required profit margin from that product at a particular selling price.What is the difference between coproduct and byproduct?

A by-product is a material that is not a primary product of a production process and is not solely or separately produced by the production process, whereas a co-product is produced for the general public's use and is ordinarily used in the form produced by the process (Section 261.1(c)(3)).Are all future costs are relevant in decision making?

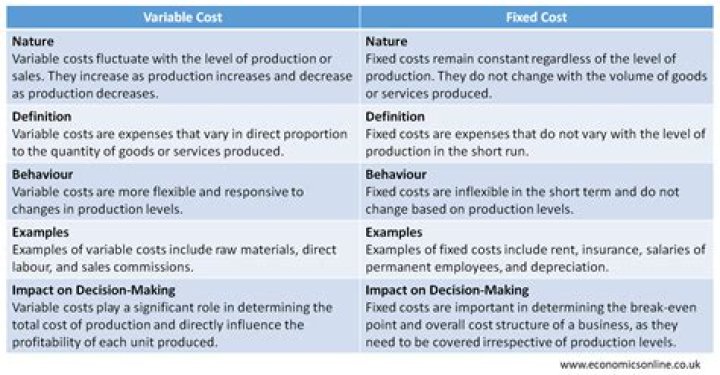

The costs which should be used for decision making are often referred to as "relevant costs". a) Future: Past costs are irrelevant, as we cannot affect them by current decisions and they are common to all alternatives that we may choose.Are fixed costs always irrelevant?

Generally speaking, most variable costs are relevant because they depend on which alternative is selected. Fixed costs are irrelevant assuming that the decision at hand does not involve doing anything that would change these stationary costs.How do you calculate cost plus pricing?

The cost-plus pricing formula is calculated by adding material, labor, and overhead costs and multiplying it by (1 + the markup amount). Overhead costs are costs that can't directly be traced back to material or labor costs, and they're often operational costs involved with creating a product.What is meant by relevant costs?

A relevant cost is a cost that only relates to a specific management decision, and which will change in the future as a result of that decision. The relevant cost concept is extremely useful for eliminating extraneous information from a particular decision-making process.Are variable costs always relevant cost?

To explain: That the variable costs are always relevant cost. Explanation:Relevant costs are those costs which are increased or decreased from its current level. Variable cost is relevant cost it there is any increment or decrement from its current level otherwise variable cost is not said to be relevant cost.What is the danger in allocating common fixed costs?

Explanation:The danger in allocating common fixed costs among products and segments of an organization can summarized as follows:(a) It would bias the breakeven point calculation for the products or segments. (b) There may not be proper basis for the common fixed costs allocation.What is differential cost?

Differential cost is the difference between the cost of two alternative decisions, or of a change in output levels. The concept is used when there are multiple possible options to pursue, and a choice must be made to select one option and drop the others.When a company has a production constraint?

When a company has a production constraint, the product with the highest contribution margin per unit of the constrained resource should be given highest priority. Managers should not authorize working overtime at a work station that contains a bottleneck.Which of the following terms is correct for a cost that has already been incurred and Cannot be changed by any decision?

A sunk cost is a cost that has already been incurred and that cannot be changed by any future decision. No. Not all fixed costs are sunk - only for which the cost has already been irrevocably incurred.How do you allocate costs?

If so, a number of possible allocation methods have been used, including: Sales. Costs are apportioned based on the net sales reported by each entity.Cost allocation methods

- Direct labor. Overhead is applied based on the amount of direct labor consumed by a unit of production.

- Machine time.

- Square footage.