How many principles of economics are there

Christopher Lucas

Christopher Lucas There are 10 basic economic principles that make up economic theory and act as a guide for economists. Aside from standard economic concepts like supply and demand, scarcity, cost and benefits, and incentives, there are an additional 10 principles to follow in the field.

What are the 7 principles of economics?

- Step 1: Scarcity Forces Trade-Off.

- Step 2: Cost versus benefits. …

- Step 7: Future consequences count.

- Step 5: Trade makes people better off. …

- Step 3: Thinking at the Margin.

- Step 6: Markets Coordinate Trade.

- Step 4: Incentives Matter.

What are the 9 principles of economics?

- People Act. …

- Every Action Has a Cost. …

- People Respond to Incentives. …

- People make decisions at the margin. …

- Trade makes people better off. …

- People are Rational. …

- Using markets is costly, but using government can be costlier still.

What are the 4 principles of economics?

The four principles of economic decisionmaking are: (1) people face tradeoffs; (2) the cost of something is what you give up to get it; (3) rational people think at the margin; and (4) people respond to incentives.What are 3 principles of economics?

The essence of economics can be reduced to three basic principles: scarcity, efficiency, and sovereignty. … They are basic principles of human behavior. These principles exist regardless of whether individuals live in market economies or planned economies.

What are the 6 principles of economics?

- People economize. …

- All choices involve cost. …

- People respond to incentives. …

- Economics systems influence individual choices and incentives. …

- Voluntary trade creates wealth. …

- The consequences of choices lie in the future.

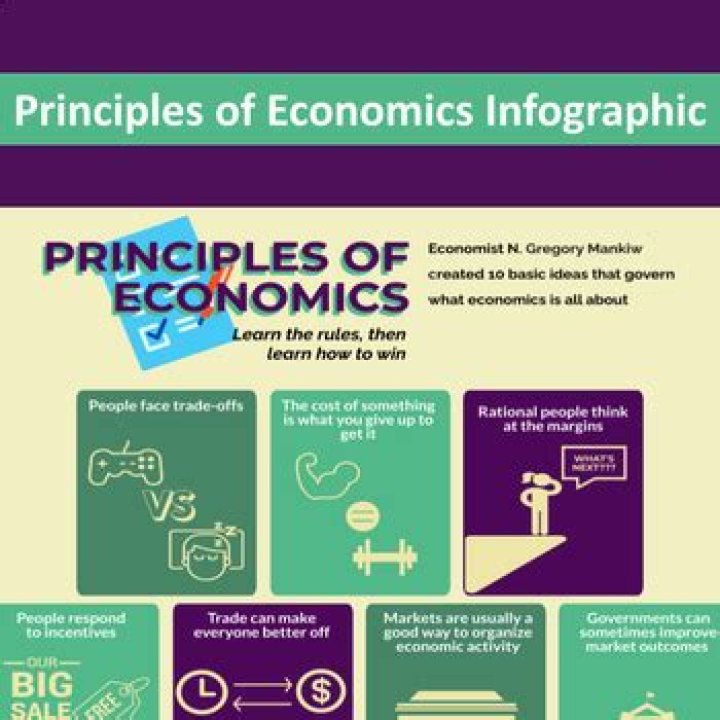

What are the 10 economic principles?

- People face trade-offs. …

- The cost of something is what you give up to get it. …

- Rational people think at the margin. …

- People respond to incentives. …

- Trade can make everyone better off. …

- Markets are usually a good way to organize economic activity. …

- Government can sometimes improve market outcomes.

What are the 4 principles of decision making?

In life there are essentially four decision making principles that give us an idea about how much influence we can have in different situations. These four principles are: Given, Input, Negotiate and Self. Many things in life can cause us distress.What are the 5 principles of economics?

There are five basic principles of economics that explain the way our world handles money and decides which investments are worthwhile and which ones aren’t: opportunity cost, marginal principle, law of diminishing returns, principle of voluntary returns and real/nominal principle.

What are economic principles?What Is the Economic Principle? … Generally speaking, it encompasses a wide variety of economic laws and theories that define or explain how an economy attempts to satisfy the unlimited demand in the marketplace with a finite supply of resources available. Thusly, some choices and trade-offs must be made.

Article first time published onWhat is the first economic principle?

A first principle underlying many economic models is that, in the round, consumers behave rationally and will always chase down the optimal result. … Traditional economic models suggest that they should have.

Who wrote the book Principles of Economics?

From 1891 to 1894 he was a member of the Royal Commission on Labour. Alfred Marshall, whose Principles of Economics (first published in 1890) was for long an authority for English-speaking… Marshall’s Principles of Economics (1890) was his most important contribution to economic literature.

What is the 5th handy dandy guide principle?

When the rules change incentives change; when incentives change choices change. 5. Voluntary trade creates wealth. … The consequences of choices lie in the future.

What is the most important principle of economic reasoning?

Scarcity exists and it doesn’t go away. Because resources are limited, people must make choices. People choose the alternatives that they perceive to offer the greatest excess of benefits over costs.

What is basic economic principle of choice?

Choice refers to the ability of a consumer or producer to decide which good, service or resource to purchase or provide from a range of possible options. Being free to chose is regarded as a fundamental indicator of economic well being and development.

What are the 8 ethical principles?

This analysis focuses on whether and how the statements in these eight codes specify core moral norms (Autonomy, Beneficence, Non-Maleficence, and Justice), core behavioral norms (Veracity, Privacy, Confidentiality, and Fidelity), and other norms that are empirically derived from the code statements.

Who presented four principles?

The Four Cardinal Principles (simplified Chinese: 四项基本原则; traditional Chinese: 四項基本原則; pinyin: Sì-xiàng Jīběn Yuánzé) were stated by Deng Xiaoping in March 1979, during the early phase of Reform and Opening-up, and are the four issues for which debate was not allowed within the People’s Republic of China.

What are economic principles and indicators?

An economic indicator is a piece of economic data, usually of macroeconomic scale, that is used by analysts to interpret current or future investment possibilities. … Such indicators include but aren’t limited to: The Consumer Price Index (CPI) Gross domestic product (GDP) Unemployment figures.

Who is called as father of economics?

Adam Smith was an 18th-century Scottish economist, philosopher, and author who is considered the father of modern economics. Smith argued against mercantilism and was a major proponent of laissez-faire economic policies.

How Robbins define economics?

In his landmark essay on the nature of economics, Lionel Robbins defined economics as. “the science which studies human behaviour as a relationship between ends and scarce means which have alternative uses” (Robbins, 1935, p.

What is Alfred Marshall's theory?

Marshall’s Principles of Economics (1890) was his most important contribution to economic literature. … In this work Marshall emphasized that the price and output of a good are determined by supply and demand, which act like “blades of the scissors” in determining price.

Are markets a good way of organizing economic activity?

Mankiw’s sixth principle of economics is: Markets are Usually a Good Way to Organize Economic Activity. … As a result of the decisions that buyers and sellers make, market prices reflect both the value of a good to society and the cost to society of making the good.

How does trade increase wealth?

How does trade create value? 1.) When individuals engage in voluntary exchange, both parties are made better off. … By channeling goods and resources to those who value them most, trade creates value and increases the wealth created by a society’s resources.

How are individual choices impacted by economic systems?

Economic Systems Influence Individual Choices and Incentives: People cooperate and govern their actions through both written and unwritten rules that determine methods of allocating scarce resources. These rules determine what is produced, how it is produced, and for whom it is produced.

What is Adam Smith's main idea?

Adam Smith was among the first philosophers of his time to declare that wealth is created through productive labor, and that self-interest motivates people to put their resources to the best use. He argued that profits flowed from capital investments, and that capital gets directed to where the most profit can be made.